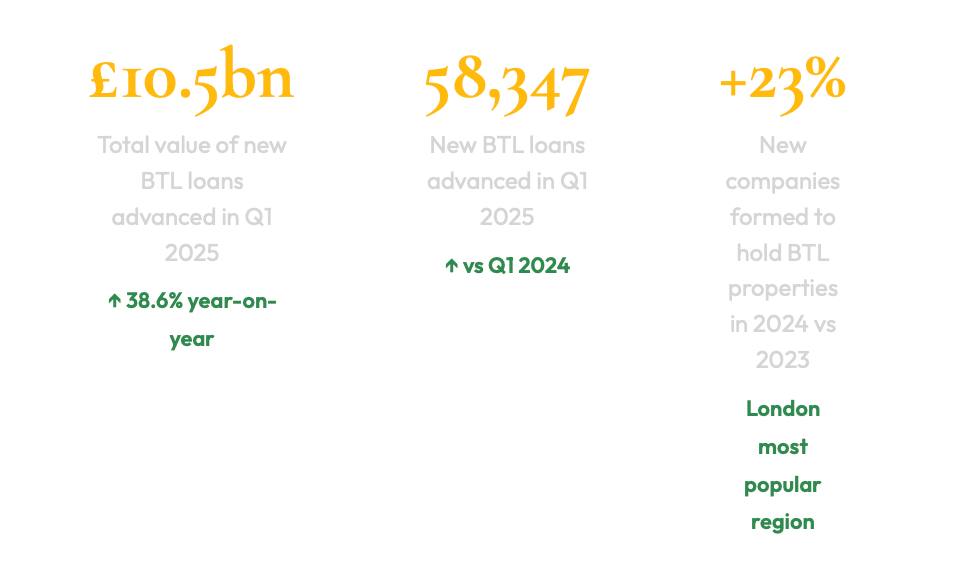

The UK buy-to-let market is rapidly transforming. Rising costs, tighter lending criteria and sweeping tax changes have reshaped the landscape — yet BTL lending hit £10.5bn in Q1 2025 alone, a 38.6% year-on-year increase.

Here is what investors need to understand right now.

It is undeniable that the UK buy-to-let market is changing at pace. For investors willing to understand the new landscape rather than retreat from it, the opportunities remain significant — and in some respects, more accessible than at any point in recent years. This article sets out the key challenges, the data behind the market’s continued resilience, and what it all means for overseas investors in 2025 and beyond.

What Is Buy-to-Let?

Buy-to-let (BTL) investment refers to the purchasing of property for the specific purpose of renting it out. The most common BTL properties are residential homes including flats and house shares. For many investors, it has historically been one of the most accessible routes to generating passive income and building long-term capital — particularly in a market as structurally undersupplied as the UK’s.

At its core, a BTL investment works by generating rental income that covers mortgage costs and operating expenses, while the property itself appreciates in value over time. The combination of income yield and capital growth has made UK buy-to-let a consistent choice for both domestic and international investors for decades.

The Market in Numbers: Q1 2025

Despite the challenges widely discussed in the market, the headline data tells a striking story of continued investor activity.

These figures point to a market that is not contracting but restructuring. Smaller individual landlords face genuine pressure — but institutional-style investors and overseas buyers are filling the gap, often through limited company structures that offer both tax efficiency and portfolio scalability.

Why Are Limited Companies Growing?

The 23% increase in BTL companies formed in 2024 reflects a deliberate tax planning response. Purchasing through a limited company allows investors to deduct mortgage interest as a business expense — an advantage removed from personal ownership by Section 24. For investors building portfolios of multiple properties, the company structure has become the preferred vehicle.

The Challenges Reshaping the Market

The UK buy-to-let landscape has faced a significant accumulation of headwinds over the past five years.Understanding each one is essential for any investor entering or expanding in the market.

The Bank of England Base Rate

The Bank of England base rate remains one of the most consequential variables for BTL investors. Although there have been meaningful reductions since August 2024, rates remain significantly higher than the near-zero levels seen in 2020–2021. For landlords on tracker or variable-rate mortgages, the cost of finance has risen substantially — compressing net yields and, in some cases, prompting exits from the market. However, the direction of travel is positive. Fixed-rate BTL products have become more competitive as lenders price in expected further reductions, and the easing cycle provides a constructive backdrop for investors entering now rather than at the 2022–2023 peak.

Section 24 and the Tax Environment

Section 24, implemented progressively from 2017 and fully in force from 2020, removed the right for individual landlords to deduct mortgage interest costs from rental income before calculating tax liability. Instead, tax is calculated on gross rental income, with only a 20% basic rate tax credit applied to mortgage interest payments. In practical terms, this significantly increased the effective tax. rate for higher- and additional-rate taxpayers who own BTL properties personally. It is the primary driver behind the growth in limited company purchases, where mortgage interest remains fully deductible as a business expense.

Section 24 — The Key Impact

Under Section 24, a higher-rate taxpayer with £15,000 rental income and £10,000 mortgage interest no longer pays tax on £5,000 of profit. They pay tax on the full £15,000, receiving Under Section 24, a higher-rate taxpayer with £15,000 rental income and £10,000 mortgage interest no longer pays tax on £5,000 of profit. They pay tax on the full £15,000, receiving

The UK Remains Attractive for

Overseas Investors

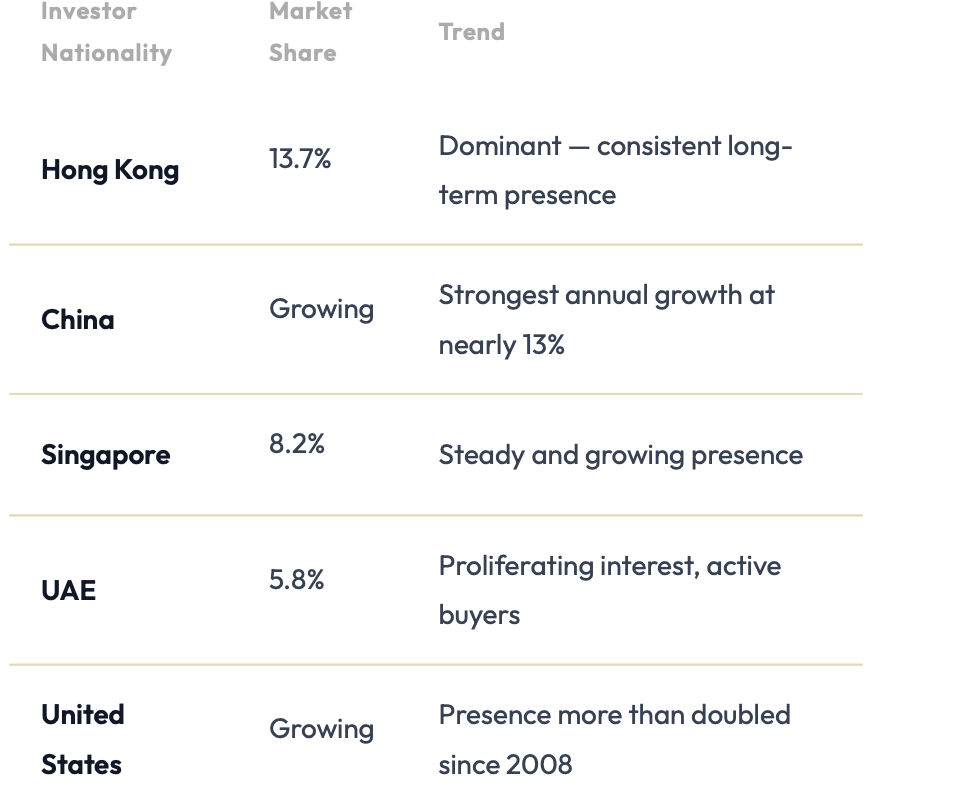

Despite the volatility of the global economic environment, the UK continues to attract significant international investment into its property market. The UK’s transparent legal framework, deep liquidity, and the strength of sterling-denominated rental income remain powerful draws for overseas buyers.

It is worth noting that while European buyers in London decreased — from 55% in 2008 to 44% following Brexit and the pandemic — this has not deterred serious long-term investors from other regions. The data suggests that short-term political events a!ect speculative buyers more than fundamental, yield-driven investors who take a longer view.

For Turkish investors specifically, the UK’s combination of sterling-denominated income, stable title system and accessible entry prices in regional cities continues to make buy-to-let a compelling addition to an international portfolio.

The role of experienced brokers and financial consultants becomes increasingly important in navigating this evolving landscape — ensuring investors access the right structures, the right lenders, and the right markets from the outset.

Frequently Asked Questions

What is buy-to-let (BTL) investment?

Buy-to-let refers to purchasing property specifically to rent it out. The most common BTL properties are residential homes including flats and house shares. It has historically been an attractive route to passive income and long-term capital appreciation — and remains so for investors who structure their approach correctly in 2025.

Is the UK buy-to-let market still growing in 2025?

Yes. In Q1 2025, there were 58,347 new BTL loans advanced in the UK, valued at £10.5bn — a 38.6% increase on the same quarter in 2024. Despite tax changes and higher mortgage rates, new lending volumes demonstrate continued investor confidence. The structure of investment is changing — towards limited companies and regional cities — but the market itself continues to grow

What is Section 24 and how does it affect landlords?

Section 24, fully implemented in 2020, removed the right for individual landlords to deduct mortgage interest from rental income before calculating their tax liability. Tax is now assessed on gross rental income, with only a 20% basic rate credit applied to interest costs. This significantly increased the effective tax burden for higher-rate taxpayers. Many investors have responded by purchasing through limited companies, where mortgage interest remains fully deductible.

Can overseas investors — including Turkish buyers — participate in UK BTL?

Yes. The UK imposes no nationality or residency restrictions on property ownership. Turkish buyers and other overseas nationals can purchase BTL properties, obtain BTL mortgages through specialist lenders, and benefit from the same legal protections as domestic investors. A non-resident stamp duty surcharge of 2% applies. Inceo Capital connects overseas investors with FCA- authorised mortgage brokers and manages the process in Turkish from end to end.

Which UK cities o!er the best buy-to-let yields in 2025?

Outside London, cities including Liverpool (7–9%), Nottingham (7%+), Manchester (7-9%), Birmingham (7-9%) and Leeds (6-7%) offer the strongest gross yields in 2025. London delivers lower gross yields (3–5%) but stronger long-term capital appreciation. The right choice depends on your investment objective income, growth or a combination of both.

Inceo Capital is not authorised by the Financial Conduct Authority, and does not provide advice on regulated mortgage or consumer credit products. All services relate to non-regulated business and investment finance, including bridging loans, buy-to-let-finance and commercial funding.